By Rachel Lyngaas, Chief Sanctions Economist, U.S. Department of Treasury

Putin is feeling the impacts of his war in Ukraine. Sanctions and export controls are damaging Russia’s economy and limiting its access to the financing and material goods needed to wage its illegitimate war of choice.[i] The United States and our partners have targeted Russia’s primary revenue drivers and access to defense materials, asymmetrically inflicting harm while minimizing unintended spillovers. While Russia has the resources to maintain its war in the short-term, its leaders face increasingly painful tradeoffs that will sacrifice long-term prospects — as underinvestment, slow productivity growth, and labor shortages will only deepen.

There are three major forces acting in concert upon the Russian economy: the war itself, U.S. and partners’ sanctions and related measures, and the Russian government’s policy response to those measures. As a result of these forces, the Russian economy is reorienting away from private consumption and towards defense spending at the expense of Russian citizens, who will face a long-term decline in living standards.

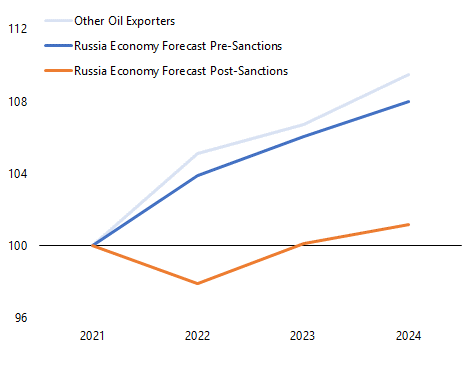

Following its invasion of Ukraine and the imposition of U.S. and partners’ sanctions and other economic measures, Russia’s economy in 2022 contracted by 2.1 percent (Figure 1),[ii] with record-high energy exports cushioning what would have been a far deeper contraction. Russia’s economy is over 5 percent smaller than had been predicted prior to the escalation, and it is far underperforming other energy exporters (including the United States). The war and associated multilateral sanctions are putting Russia’s economy under considerable economic strain, contributing to rapidly growing expenditures, a depreciating ruble, increasing inflation, and a tight labor market reflecting a loss of workers.

Figure 1. Real GDP vs. Counterfactual – 2021=100

Sources: IMF and Treasury staff calculations. Pre-escalation Russian trajectory is the IMF’s 2021 Article IV forecast; the war economy trajectory is the October 2023 IMF WEO. Comparison countries are oil exporters: Brazil, Canada, United States, Saudi Arabia, Mexico, Iraq, the UAE, Norway, and Kuwait.

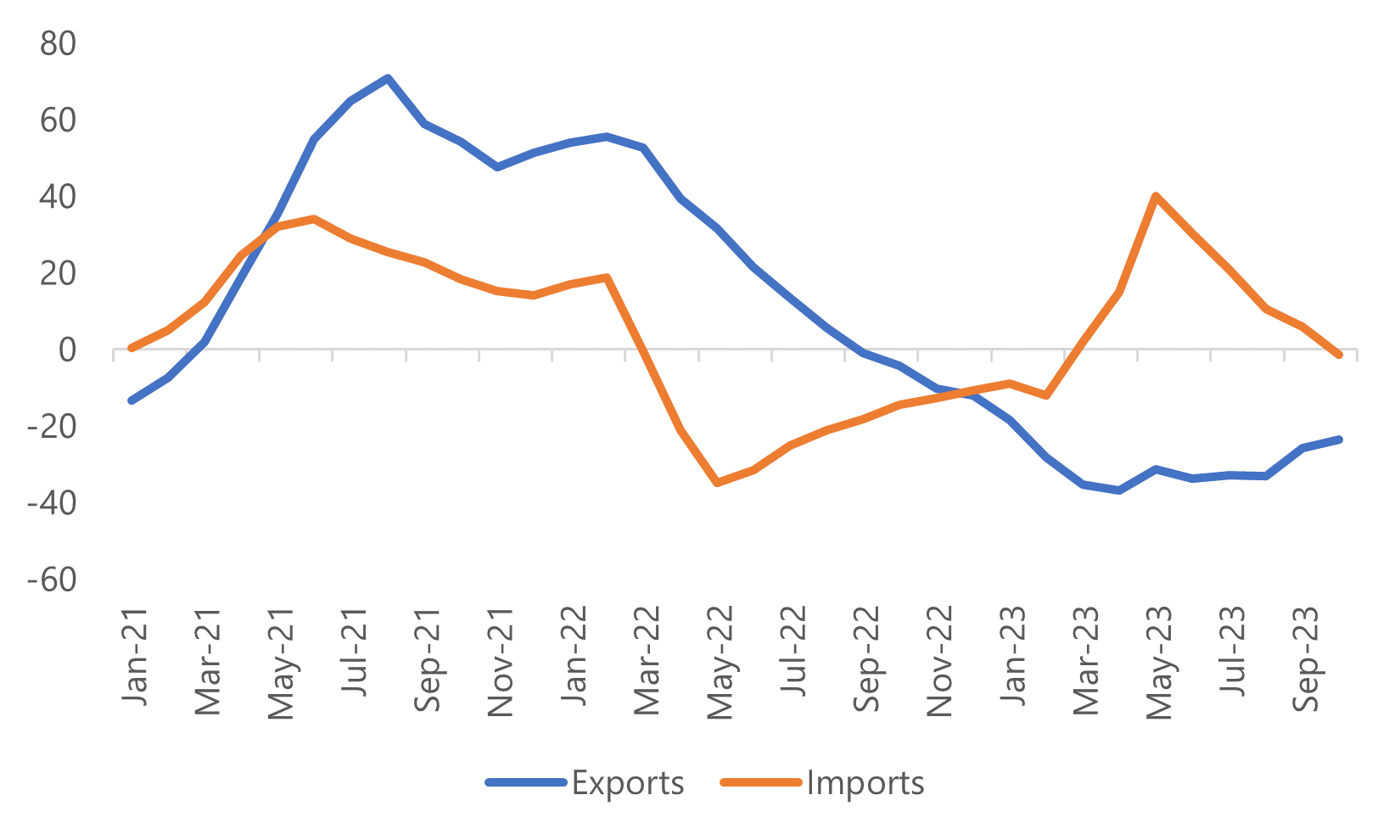

The United States and partners’ imposition of financial sanctions, export controls, the EU crude oil embargo, and the Price Cap on Russian oil[iii] have combined to make it more difficult for Russia’s war industry to source key high-tech components and other needed intermediate inputs. The decline in Russia’s 2022 growth was driven by a 14 percent contraction in exports and 11 percent decline in imports over 2021, among other factors (Figure 2). As a result, Russia has pursued a costly realignment of its supply chains to import lower-quality substitutes from third countries. Russia has also struggled to access key inputs needed for its war due to U.S. and partners’ sanctions and export controls that limit its access to key technologies. Russia cannot yet domestically manufacture these advanced weapons – the United States and its partners are taking actions to help ensure that it never does. Russia is now more isolated, relying on individuals and entities willing to resupply its military and perpetuate its heinous war against Ukraine. The United States imposed sanctions last month to hold these actors accountable, in measures that will further constrain Russia’s ability to acquire technology and equipment to wage its war.[iv]

Figure 2: Real Russian Trade Flows – Y/y % change

Source: Russian Central Bank and Treasury staff calculations. Three-month rolling average of monthly Imports and Exports of Goods and Services, valued in USD and adjusted for inflation.

Emigration: Russia’s People Are Voting with Their Feet

The economic outlook for Russian households has soured. An uptick in emigration predated Russia’s full-scale invasion of Ukraine, but the war mobilization effort in 2022 accelerated the trend in young and educated people leaving for opportunities abroad.[v] As Russia mobilized its war effort, emigration has reached historic highs; around 668,000 people left Russia in 2022 — a 71 percent increase over the prior five-year average (Figure 3). In the long-term, this permanent loss in human capital with further weaken Russia’s growth potential; the Russian government is acutely aware of this, offering subsidized mortgages to get skilled workers to stay.[vi]

Figure 3. Emigration Patterns – 1000s departing (all persons)

Sources: Russia Federal State Statistics Service and Treasury staff estimates.

Note: 2023 estimates include a lower bound (orange bar), based on average monthly emigration through August 2023 and an upper bound (gray bar) based on the maximum monthly emigration values reported in 2023.

Foreign Exchange: A Weak Ruble

The Russian economy has also experienced volatility in its exchange rate, with the ruble falling then rising then falling again, now down roughly 20 percent against the dollar from early February 2022 to December 2023 (Figure 4). This depreciation, while not a measure of the efficacy of sanctions, does impact Russia’s fiscal balance and has made Russia’s imports more expensive, which – alongside other restrictions imposed by the United States and its partners — make Russia’s ability to acquire war materials more difficult.

Figure 4. Value of Ruble – Ruble per USD

Sources: Russian Central Bank and Treasury staff calculations

FISCAL OUTLOOK: DIMINISHING ROOM TO SPEND

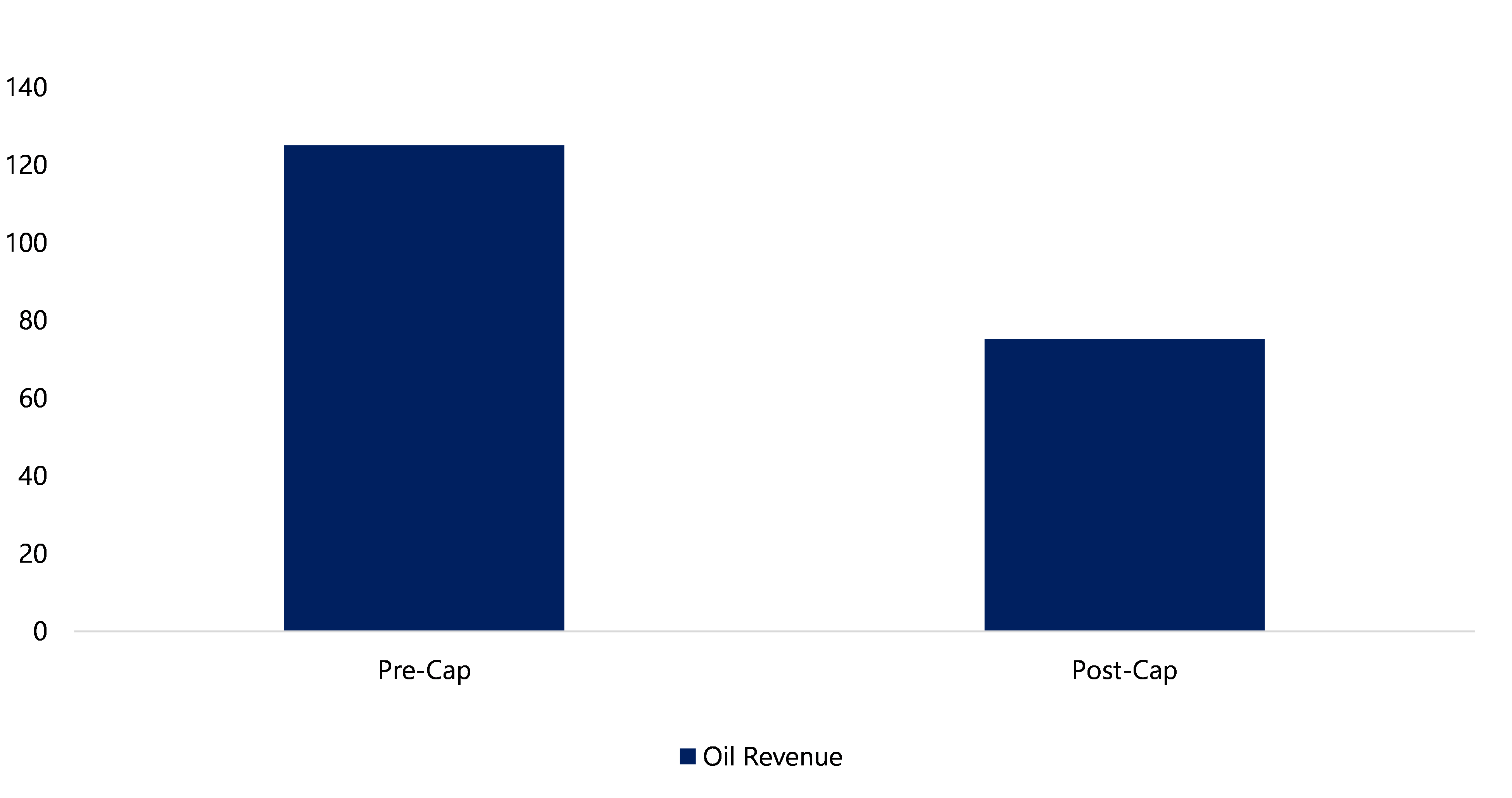

In 2023, growth in the Russian economy has been largely driven by an increase in government spending on the war in Ukraine, infrastructure, and increased social outlays. The Russian authorities have doubled the 2023 defense spending target to more than $100 billion (a third of all public expenditure) while pausing public salary increases slated for 2024. As spending has grown, energy revenues have declined sharply—by almost 40 percent from January through October 2023 relative to 2022 (Figure 5). That decline reflects many factors, including the decline in global oil prices through 2022 and much of 2023, as the targeted sanctions regimes helped avoid the significant Russian supply shock that markets feared after the invasion. Moreover, the effects of two key measures – the EU embargo and the Price Cap – helped reduce Russia’s export earnings by forcing sizeable discounts on Russian exporters in market segments where the EU embargo lowered demand.[vii] This decline in revenue increased pressure on Russia’s fiscal balance, given that oil and gas tax revenue are key sources of Russia’s revenue. Of course, the rise in global oil prices since Summer 2023 allowed some recovery in Russia’s revenues; but increased enforcement of the price cap and related sanctions regimes[viii] continue to limit revenues.

Figure 5. Oil and Gas Federal Budget Revenue, pre- and post- Price Cap – (USD billions)

Sources: Russian Ministry of Finance and Treasury staff calculations. Revenue includes mineral extraction tax and oil export duty, Jan. – Oct. 2022 compared to Jan. – Oct. 2023.

The Russian government has undertaken several policy responses to fill fiscal gaps, including changes to tax policy and utilization of the National Wealth Fund’s (NWF) fiscal reserves, but these all come at a cost. Disbursals from the NWF, windfall taxes, and domestic debt issuances are covering the deficit in the near-term, but the combination of increased use of the NWF and multilateral sanctions are depleting it; the NWF currently holds about $146 billion, nearly half of which ($72 billion) is in gold and liquid yuan assets. The immobilization of around $280 billion in Russian reserves in the NWF and Central Bank sovereign assets by U.S., EU, and partner sanctions (roughly half of total foreign reserves pre-war) leaves Russia without access to an important buffer. As a result of monetary financing and other factors — including a tight labor market — annual inflation stands at 7.5 percent as of end-November and Russia’s Central Bank projects it to reach 7.0–7.5 percent by the end of the year, well above its 4 percent target. Inflation may continue to rise as sources of nonmonetary finance dwindle.

RUSSIAN POLICY CHOICES – HARDER AND INCREASINGLY EXPENSIVE

The Russian government has consistently prioritized stop-gap measures over long-term prosperity. The increase in defense-related spending, for example, coincided with a decline in total household consumption by approximately 2 percent in 2022. Moreover, with efforts by the Central Bank to slow inflation — ultimately increasing the benchmark interest rate to 15 percent — borrowing and investment costs have become more expensive for both citizens and the government.

The consequences of Russia’s war have forced it to retreat from global markets, making it more vulnerable to the demand changes of a smaller group of partners. Pulling back from global markets also restricts Russia’s ability to access new ideas and innovations. Without ready access to these key drivers of long-term growth (including FDI, which has been net negative since February 2022, Figure 6), the Russian economy is primed to fall into a weaker, less productive trajectory. The costs are now higher for Russia to further develop its energy infrastructure and invest in projects that would generate future revenue. For example, the Nord Stream 2 natural gas pipeline cost Russia and its investors over $11 billion and is now abandoned: alternative projects will face steeper costs and investors will be more timid, given the unreliable nature that Russia has revealed. As the world shifts more to investments in renewable alternatives, Russia faces more uncertainty and additional costs that cloud its long-term prospects.

Figure 6. Foreign Direct Investment in Russia (billions of USD)

Source: Russian Central Bank.

PROTECTING THE GLOBAL ECONOMY: MITIGATING SPILLOVERS

Actions taken by the United States, whether on our own or with our partners, have been carefully calibrated to mitigate costs from Russia’s war of choice on the global economy:

- Price Cap: The price cap on Russian oil aims to curtail Russian profits while keeping oil supply stable by forcing Russia to sell its oil cheaper than it otherwise would. At the start of its invasion, Russia received windfall profits on an oil price spike created by its own war of choice. A persistent price spike from reduced global oil supply would have been disastrous for the low- and middle-income countries that rely on Russian oil. The price cap policy works to maintain oil market stability by keeping Russian exports on the market, while limiting Russia’s ability to profit on that oil. The price cap works by requiring any sale of Russian oil that involves companies, such as insurance or flagging companies, based in coalition countries to be sold under the price cap level. Treasury and its international partners have recently imposed price cap-related sanctions on entities and identified vessels as blocked property for carrying Russian oil priced above the price cap.

- Food Security: The United States has not imposed sanctions related to Russian agricultural commodities or equipment. To counter Russia weaponizing hunger, the United States has supported the Black Sea Grain Initiative that helped approximately 33 million metric tons of grain reach global markets, driving down food prices around the world. Nearly two-thirds of the wheat exported through that deal went to developing countries. Not only did Russia pull out of the deal on July 17, 2023, but it is now mining Ukraine’s fields, bombing its ports and rails, and burning its silos. The United States continues to work with allies and partners to safeguard global food security and bring grain to the world market.

- European Gas: President Biden committed to help Europe access liquefied natural gas. Allies and partners, especially in Asia, allowed these energy resources to be directed to Europe as part of this global effort to ensure the EU’s access to energy. The United States acted quickly to restrict Russia’s ability to gain revenues through its oil and gas sector, including by announcing prohibitions on Russian liquified natural gas imports within weeks of the start of the war. The United States remains committed to supporting Europe’s energy goals, including through the U.S.-EU Task Force on Energy Security.

Source : Home Treasury